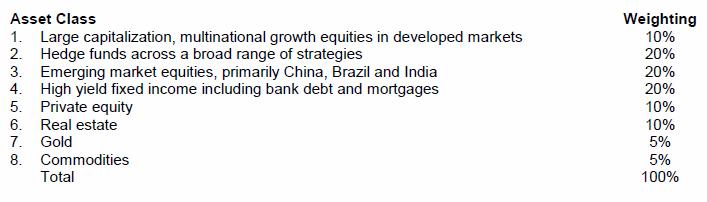

This month BlackRock shared Byron Wein’s views on asset allocation in their December Commentary. Wein’s piece was titled, “A Radical Approach to Asset Allocation.” Indeed it is. The following is Wein’s recommended asset allocation for U.S. investors:

Here the big news is that traditional large cap global growth stocks only comprise 10% of Wein’s portfolio. Alternative investments like hedge funds, private equity, real estate, gold, and commodities make up 50% of the total. Emerging market equity at 20% and high yield fixed income at 20% comprise the rest of the portfolio. Clearly Mr. Wein is not bullish on the prospects for global corporations to grow their earnings.

To me, these asset allocations are interesting but not necessarily relevant to the question at hand. I want to know what circumstances would cause either pundit to change their allocation. If stocks lose 50% of their value would Wein still only rebalance to 10% of his portfolio? If real estate trusts double in value would Professor Malkiel still own 12% in these securities? Both Malkiel and Wein offer portfolio allocations that are rather predictable in light of the past decade’s awful U.S. equity performance. They both look in the rearview mirror to come up with an allocation that is presumed to have meaning to intelligent investors regardless of the facts and circumstances of future market environments. As far as I’m concerned, these allocations are relevant until they are not. When the facts and circumstances of the global economy change, these allocations should be changed as well. That’s what we call tactical asset allocation.